What the Latest IFC Report Reveals About the State of Impact Investing

Senior Manager, Content Marketing & Storytelling at MovingWorlds

on September 8, 2021 / Alexandra Nemeth

Impact investing is a hot topic in the social impact space right now. But what exactly is impact investing, and how is it different from other investing? Put simply, it comes down to intent. Traditional investing is done with the single goal of maximizing financial returns. Impact investing, however, is defined as investing into companies and organizations with the intent to contribute to measurable positive social or environmental impact alongside financial returns.

This marks a meaningful shift away from the shareholder primacy model of capitalism and towards a more equitable new normal that takes a much broader range of stakeholders into account. And although it’s still relatively small, this market has the potential to make real progress towards the Sustainable Development Goals (SDGs.)

The International Finance Corporation (a division of the World Bank Group) recently published a comprehensive report exploring how the impact investing market has grown, evolved, and where it’s headed. Find the key takeaways about the current state of impact investing below!

The pandemic made impact investing even more popular

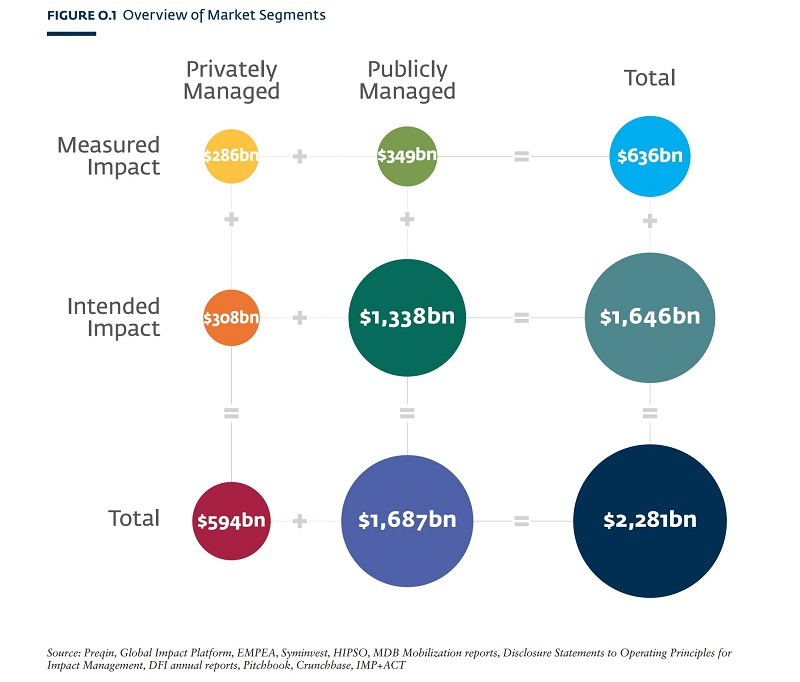

Collectively, up to $2.281 trillion might have been invested for impact by the end of 2020. This growth is despite the disruption and uncertainty brought on by COVID-19. According to the report, “Impact investing has seen a boost in popularity due to heightened awareness of social challenges such as unequal access to healthcare and racial and gender inequality, as well as increased attention to the effects of climate change. 2020 also marked a profound shift in the way institutions invest, as many investors have recognized that companies with strong ESG practices outperformed during the pandemic.”

The graphic above shows the breakdown of the total impact investing market based on whether the assets are publicly or privately managed, and whether investments are ‘measured impact’ or ‘intended impact.’ As we elaborate on in this video, impact measurement exists on a spectrum, with different levels of rigor. And that’s the case for impact investments, too. We’ll share more about the difference between measured and intended impact in the next section.

Impact investing has become more mature over the last year, particularly in terms of measured impact

You can think of measured impact investments as the most rigorous – these investments meet the 3 conditions of:

- Intent (credibly managed with intent for positive impact)

- Contribution (have an identifiable contribution to that impact), and

- Measurement (have a measurement system in place to quantify the impact).

Intended impact investments also satisfy the same intent condition, but do not observably or credibly satisfy both the contribution and measurement conditions.

In 2019, only $505 billion of investments were identified as measured impact assets. But in 2020, measured impact investments totaled $636 billion – representing a 25% increase in just one year. It is worth noting that impact investments actively measured for impact are still a fraction of the total so-called impact investments, and we expect that active measurement will increase as measurement practices become more consistent and more solutions lower the cost of doing so.

There is more, higher quality information available about impact investments

Impact investing is still relatively new, and there isn’t yet a universal set of standards for regulating, reporting, or monitoring on impact investments. That made it tricky to answer the question: “Is this really an impact investment, or is this greenwashing?”.

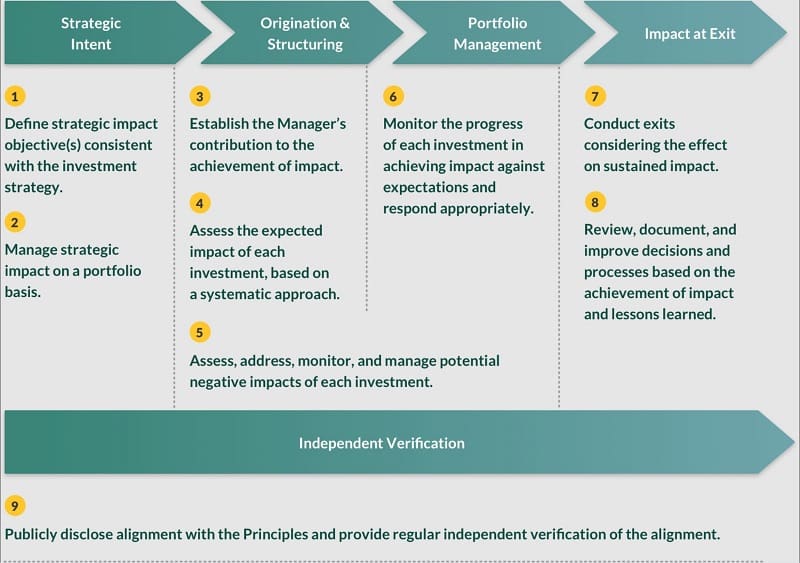

To help remedy that, in 2019, the Operating Principles for Impact Management (aka “Impact Principles”) were established as a framework to guide investors in the design and implementation of their impact management systems, ensuring that impact considerations are integrated throughout the investment lifecycle (not just in the marketing.) You can read more about the 9 impact investing principles here and see a summary in the graphic below:

Signatories to the Impact Principles are impact investors that publicly demonstrate their commitment to implementing a global standard for managing investments for impact. As of May 31, 2021, 97 of the signatories to Impact Principles have published their disclosure statements, which constitutes half of measured impact assets under management. That means that less than two years after the Principles were implemented, half of measured impact investments now have publicly available and verifiable information on exactly how they are making an impact.

Sure, we still have a ways to go, but these are encouraging signs. In 2020, there were 46 new signatories to the Impact Principles, bringing the total up to 97 at the time of the report’s publication and 137 today. The sharp increase in both the volume and quality of information available about these investments demonstrates an increase in both accountability and transparency – something crucial to achieving impact at scale.

Issuance of green, social, and sustainability bonds in public markets have also increased

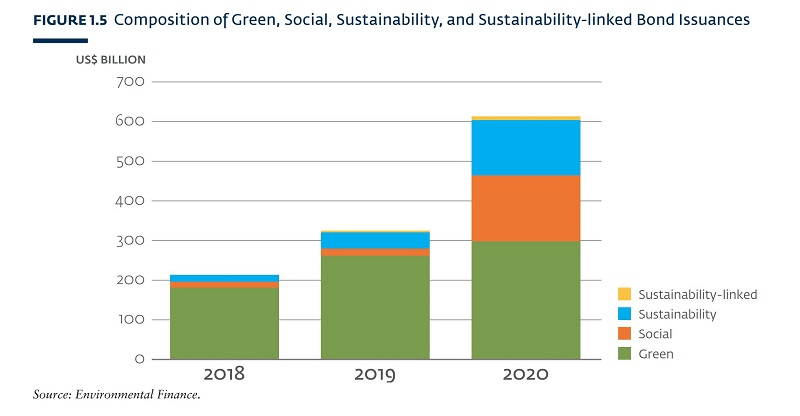

Another trend worth noting is the rise of the public impact investing market, which at a size of $95 trillion dwarfs private markets we’ve been talking about so far. According to the report, “In the public markets, various assets saw a significant increase in issuance in 2020. Social bond issuances increased eightfold over 2019, sustainability bond issuances increased by a factor of three over 2019, and green bonds broke $1 trillion in cumulative issuances.”

Why is that significant? To varying degrees, these Green, Social, & Sustainability (GSS) bonds restrict what the money invested can be spent on – ie social and environmental impact, NOT extractive industries. The figure below highlights the tremendous growth that has happened in this space in the last year:

In 2020, the GSS market saw an 87 percent increase over 2019. That increase in volume also came with an increase in diversity, as you can see that social bonds are occupying a larger segment than ever before.

COVID-19 had a big part to play in that. The report explains, “Social and sustainability bonds have been an attractive instrument to raise assets for COVID-19 recovery projects and efforts for state-associated and private institutions alike.” Take a look at these examples from different sectors:

- Governmental: To support COVID-recovery in 2020, the European Union issued three social bonds with the intent to raise $47 billion for the European Instrument for Temporary Support to Mitigate Unemployment Risks in an Emergency (SURE).

- Financial institutions: In October 2020, Citibank issued the largest ever private sector social bond, a $2.5 billion instrument to support affordable housing, particularly for communities of color.

- Private corporations: Alphabet Inc., Google’s parent company, issued a cumulative $5.75 billion in sustainability bonds, the proceeds from which will be used to finance investments in the circular economy, black-owned businesses, affordable housing, climate action, and COVID-19 responses.

As with everything else in the impact investing world, there is still a significant amount of ambiguity and rapid pace of change. But the significant takeaway here is that the pandemic has spurred more mainstream adoption of financial instruments that take social and environmental impact into account more than ever before.

It’s going to take more than shareholder activism to replicate this on a large scale

The report explains that, “Corporate engagement and shareholder action strategies have long been a tool used by shareholders to influence the management of firms, including nudging them in the direction of more sustainable and responsible Management. Despite most S&P 500 companies publishing corporate ESG reports (90 percent in 2020, up from 86 percent in 2019 and 20 percent in the 2000s), investors are seeking more transparency and more accountability with respect to the environmental and social footprints of companies and their impact on long-term shareholder value.” It is also worth noting that just because a company issues an ESG report, it does not mean they are actively working to improve their ESG targets or contribute to the Sustainable Development Goals (We’ll be publishing a new guide on ESG soon which you can subscribe for here).

In order to achieve real impact through investing, there must be forces at work both within the market (shareholder activism to influence actions) and outside of the market (governmental and regulatory bodies making certain actions mandatory, such as in disclosures.) In some places, like in Europe, forward progress is being made: in March 2021, the European Commission imposed mandatory ESG disclosures on all EU financial market participants and advisers, including foreigners.

In other places, like the USA, not so much. In September 2020, the U.S. Securities and Exchange Commission (SEC) passed amendments to shareholder-proposal rules that “severely limit the ability of shareholders to lead resolutions on key environmental, social, and governance issues.” New SEC may take it in a different direction, but it’s the same pattern we often see when pushing for systemic change: two steps forward, one step back.

A Final note

To quote Michelle Garcia Winner and Pamela Crooke, “Good intentions are not good enough”. We are excited about the rise in impact investing assets, in both public and private markets, but also see that there must be an accelerated rate of overall market growth AND a greater shift of these assets towards measured impact. Innovations in impact measurement and reporting, along with regulatory requirements to do so, will be key to helping this sector achieve its world-changing potential.

Considering pivoting your career towards impact investing? Apply to the MovingWorlds Institute for the confidence, connections, and hands-on experience you need to break into social impact.

SOCIAL IMPACT NEWS

FOLLOW US

SCALE YOUR IMPACT

SIMILAR POSTS

-

Scaling Human Impact with AI: Four Lessons from Social Entrepreneurs on the Frontlines

Personalized social impact is finally affordable.

-

What We Learned from Winning Two Anthem Awards for Corporate Social Impact

This year, MovingWorlds was honored with two Anth

-

Making the Case for Skills-Based Volunteering: ROI Insights from EY, SAP, and MovingWorlds

Most executives believe in the business case for

-

Press Release: MovingWorlds Recognized by The 2025 Anthem Awards in Two Categories

We are excited to announce that MovingWorlds